I am an Assistant Professor at the Darden School of Business of the University of Virginia, where I teach courses in Valuation and Derivatives.

My research interests are in empirical asset pricing. I study the markets for sovereign bonds and their derivatives—in terms of pricing, arbitrage, and liquidity—focusing on the impact of central banks’ market operations.

I serve as consultant for the ECB’s Directorate General Market Operations. The views expressed on this page and in my papers are entirely my own.

You can download my CV and find more info at my Google Scholar or SSRN profile.

Publications

Sovereign Credit Risk, Liquidity, and ECB Intervention

Journal of Financial Economics, 2016, 122(1),

with Loriana Pelizzon, Marti Subrahmanyam, and Jun Uno.

Featured in Think Tank Review, 2015(23), by the Council of the European Union

Internet Appendix

We examine the dynamic relationship between credit risk and liquidity in the Italian sovereign bond market during the Euro-zone crisis and the subsequent European Central Bank (ECB) interventions. Credit risk drives the liquidity of the market: a 10% change in the credit default swap (CDS) spread leads to a 13% change in the bid-ask spread, the relationship being stronger when the CDS spread exceeds 500 bp. The Long-Term Refinancing Operations (LTRO) of the ECB weakened the sensitivity of market makers’ liquidity provision to credit risk, highlighting the importance of funding liquidity measures as determinants of market liquidity.

In Sickness and in Debt: The COVID-19 Impact on Sovereign Credit Risk

Journal of Financial Economics, 2022, 143(2)

with Patrick Augustin, Valeri Sokolovski, and Marti Subrahmanyam.

Winner of the Best COVID-19 Paper Award at the IRMC 2020, featured in Ideas to Action

Internet Appendix

The COVID-19 pandemic provides a unique setting in which to evaluate the importance of a country’s fiscal capacity in explaining the relation between economic growth shocks and sovereign default risk. For a sample of 30 developed countries, we find a positive and significant sensitivity of sovereign default risk to the intensity of the virus’ spread for fiscally constrained governments. Supporting the fiscal channel, we confirm the results for Eurozone countries and U.S. states, for which monetary policy can be held constant. Our analysis suggests that financial markets penalize sovereigns with low fiscal space, thereby impairing their resilience to external shocks.

How Sovereign is Sovereign Credit Risk? Global Prices, Local Quantities

Journal of Monetary Economics, 2022, 131

with Patrick Augustin, Valeri Sokolovski, and Marti Subrahmanyam.

Internet Appendix

The sovereign default insurance market is concentrated and strongly intermediated, with fluctuations in insurance prices being dominated by common, global sources of risk. Yet, we find that insurance quantities are primarily explained by country-specific factors. Using net positions in sovereign default insurance contracts for 60 countries from October 2008 to September 2015, we find that the stock of a country’s debt, and the size of its economy, explain 75% of cross-country differences in net insured interest. Debt issuance significantly explains variation in its dynamics. Our findings are informative for the regulatory debate on the market for sovereign default insurance.

Central Bank-Driven Mispricing

Accepted at Journal of Financial Economics

with Loriana Pelizzon and Marti Subrahmanyam.

Featured in Forbes and Ideas to Action

We show that bond purchases undertaken in the context of quantitative easing efforts by the European Central Bank created a large mispricing between the market for German and Italian government bonds and their respective futures contracts. On top of the direct effect the buying pressure exerted on bond prices, we show three indirect effects through which the scarcity of bonds resulting from the asset purchases drove a wedge between the futures contracts and the underlying bonds: the deterioration of bond market liquidity, the increased bond specialness on the repurchase agreement market, and the greater uncertainty about bond availability as collateral.

Working Papers

A Real Cost of Free Trades: Retail Option Trading Increases the Volatility of Underlying Securities

with Marc Lipson and Jiang Zhang.

Featured in Wealthmanagement.com Virtual Derivatives Seminar presentation videoWe examine the link between retail trading in options and the volatility of the underlying assets. Using Robinhood’s introduction of options as a shock to retail trading, we confirm that option volume increased around this event and show that volatility similarly increased for: interlisted US securities, relative to their Canadian counterparts; optioned shares relative to optionless shares for firms with dual class shares; and more so for shares that would be become more attractive to retail traders as a result of the fee change (relatively high stock prices or low option prices). We provide further evidence suggesting the effect is permanent and that the underlying mechanism is related to market makers hedging their option exposure: volatility increases more for shares with higher option-embedded leverage; spreads and price impacts are lower; market maker volumes increase; and the volatility of retail option volume increases. Our results suggest that a shift in retail trading toward options drives an increase in the volatility of the optioned securities due to that actions of market makers hedging their exposure.

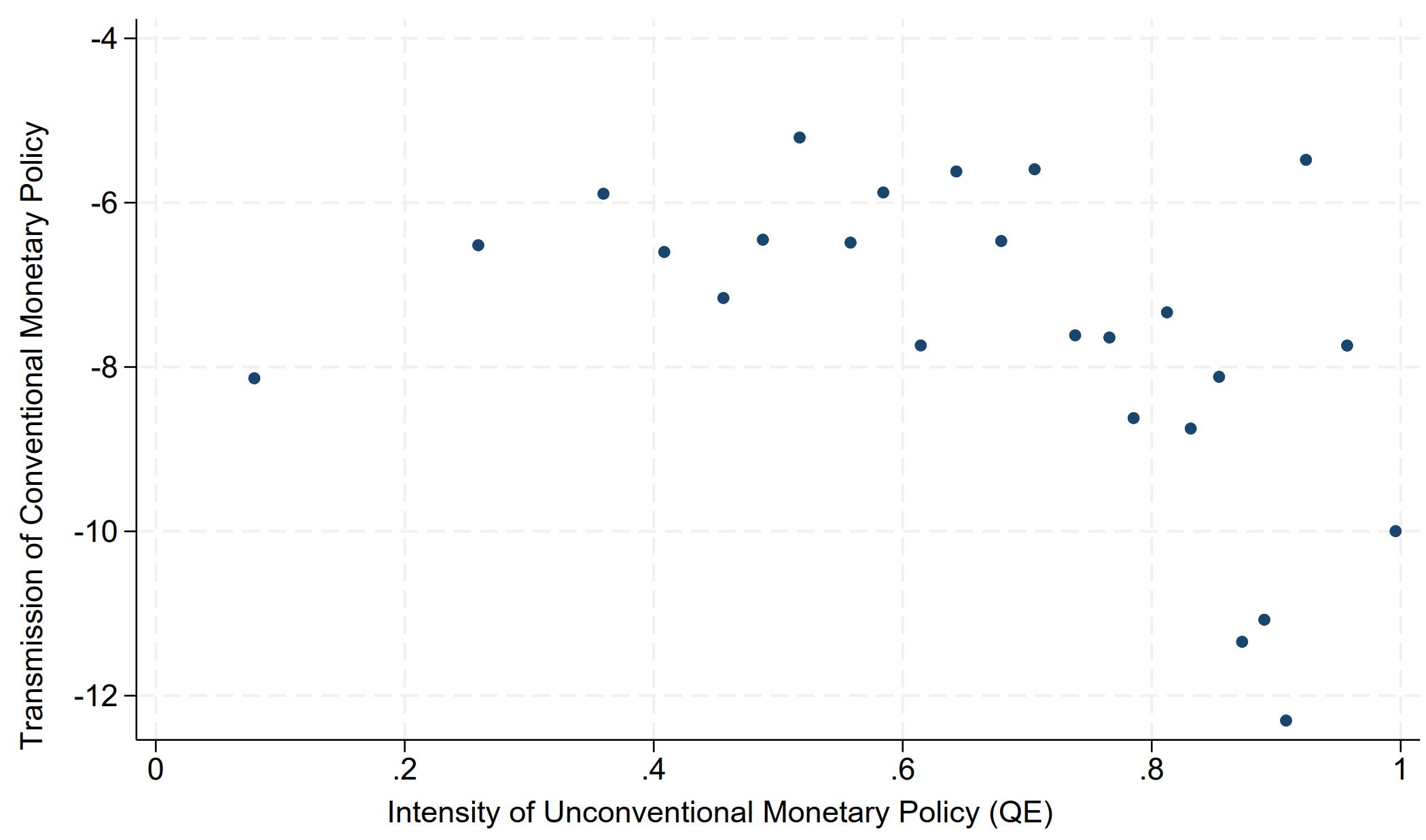

Safe Asset Scarcity and Monetary Policy Transmission

with Benoit Nguyen and Miklos Vari.

2023 ECB Money Market Conference presentation videoMost central banks exited their decade-long accommodative monetary policy cycle by first raising rates, rather than starting by reducing their balance sheet. We show that the scarcity of government bonds—which were purchased under QE and held by central banks—reduces the transmission of rate hikes to money market rates. In July 2022, when the ECB increased its policy rates by 50bp for the first time in a decade, rates of repo transactions collateralized by the scarcest bonds increased by only 30bp. We show that this imperfect pass-through to repo rates is priced in treasury yields. Heterogeneous bond holdings across institutions imply that collateralized funding costs vary significantly across European institutions.

Arbitraging Liquidity

This paper shows theoretically and empirically how arbitrage activity contributes to the convergence of liquidity across markets. Based on simple arbitrage arguments, I show theoretically how arbitrageurs’ market and limit orders create a co-movement across markets of bid prices, ask prices, and bid-ask spreads. Empirically, I document how the intensity of arbitrage activity is related to the co-movement of market liquidity between securities linked by arbitrage. I focus on Canadian stocks cross-listed in the United States and also consider commonality across stocks and corporate bonds linked by capital structure arbitrage.

The Microstructure of the European Sovereign Bond Market

with Loriana Pelizzon, Marti Subrahmanyam, and Jun Uno.

Featured in ZeroHedge

We describe the structure of the European Sovereign Bond market and document cross-sectional differences in bonds’ liquidity. We present a cohort of classical liquidity measures and relate them to the frequency of quote updates by the market makers.

Part of the analysis in this paper was included in Sovereign Credit Risk, Liquidity, and ECB Intervention

Teaching

At Darden

At CBS

Corporate Finance, BSc Course

2014-2017.

Cases

F-1978 Option Greeks, Insider Trading, and the Heinz Acquisition

CV

Download the full CV

Current Appointment

Assistant Professor of Business Administration – Darden School of Business, University of Virginia (July 2017 – Current)

Consultant – DG Market Operations, European Central Bank (November 2023 – Current)

Education

Ph.D. in Finance at the Copenhagen Business School. (2011 – 2017)

Visiting Ph.D. Student at Stern School of Business at New York University.

Visiting Ph.D. student at the Johnson Graduate School of Management at Cornell.

M.Sc. in Economics and Finance from the University of Copenhagen.

B.Sc. in Economics from the University Ca’ Foscari of Venice.

Impact

Citations

Opinion Pieces

Coronavirus is making clear there is no solidarity in the EU, Forbes, May 2020

with Patrick Augustin, Marti Subrahmanyam, and Valeri Sokolovski.

India Inc’s Rising Cost of External Capital, Business Today, July 2020

with Paolo Pasquariello and Marti Subrahmanyam.

Con i mercati sotto pressione non sempre il prezzo e giusto, Il Sole 24 Ore, July 2020

with Paolo Pasquariello and Marti Subrahmanyam.

To fight the coronavirus budget crisis, act like Alexander Hamilton, Fortune, July 2020

with Patrick Augustin, Valeri Sokolovski, and Marti Subrahmanyam.

Il serait sage pour les gouvernements fortement endettés de réduire leurs dettes dès qu’ils le peuvent, Le Monde, April 2021

with Patrick Augustin, Valeri Sokolovski, and Marti Subrahmanyam.